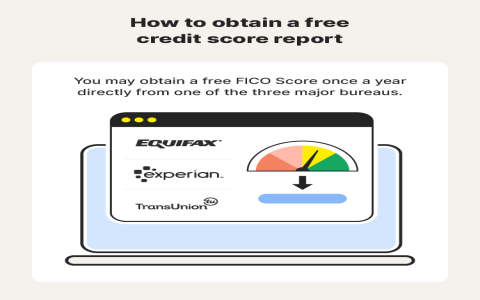

Okay, so, today, I wanna talk about how I tried to figure out my “idnscore.” To be honest, I didn’t really know what it was at first, but it sounded important. I get it that it’s like a three-digit number that lenders look at when they decide if they want to give you money. A higher score means you’re good at managing money, and a lower score… well, not so much.

So, I started by, you know, trying to find out what this score actually is. I found this tool online. And also I found some tips on a website about how to improve the score. The basic idea is to pay your bills on time and in full. That makes sense, right?

Then I went to inspect my credit report and score. And I saw that my score wasn’t as good as I hoped.

It was a bit of a bummer, but then I found this other bit of info saying it takes time to improve your score. So, I didn’t freak out.

Steps I Took

- Checked my score: This was the first step, finding out where I stand.

- Looked for ways to improve: I found some tips online, mostly about paying on time.

- Tried to understand what affects the score: This part was a bit tricky, but I got the general idea.

Realized it’s a long game: This wasn’t going to be a quick fix, and that’s okay. I set up some reminders to pay my bills, and I’m trying to be more careful with my spending. It’s a work in progress, but I’m feeling a bit more in control now. And It takes time to improve credit score.

It’s not the most exciting thing, but I thought I’d share my experience. Maybe it’ll help someone else who’s trying to figure this stuff out. If you’ve got any tips, feel free to share them. We’re all in this together, right?

{kind=link}